The Better Business Bureau is warning residents about common tax collection scams.

Consumers should be aware of unsolicited phone calls, emails or letters claiming to be from the IRS or other official-sounding government agencies.

In 2016, more than 7,500 reports came in of tax collection fraud

Among the common scams:

• Imposter scams where scammers pose as IRS agents and demand money or threaten jail time. According to the BBB, fraudsters spoof phone numbers so the call appears to be coming from the IRS or local law enforcement.

• Tax Relief Scams where deceptive ads claim to greatly reduce a person’s tax liability. Scammers use official-looking notices or websites.

• ID theft where scammers use stolen personal information, Social Security numbers and falsified W-2 information to file fraudulent tax returns in the victim’s name. In some cases, thieves stole W-2’s out of unsecured mailboxes.

Consumers can protect themselves by doing the following:

• Electronically file only from secure computers with up-to-date anti-virus software and private Wi-Fi.

• Avoid filing taxes from a link in an email.

• Mail through the post office or a secure mailbox.

• Shred information that’s more than seven years old.

• Check personal credit reports annually to ensure there are no unauthorized accounts in your name.

Your tax years are like thumbprints: No two tax years will look alike. One year you are single, and you're married the next. One year you rent and the next you buy a home. You live on the East Coast one year and then move to the West Coast.

You might have experienced some life changes in the year 2016. Here are a few possible events and how they can impact someone's income taxes:

Marriage/divorce

Did you tie the knot last year? If so, congratulations! You and your spouse can file taxes together. According to TurboTax, filing a joint tax return will give you a lower tax rate with better deductions and exemptions. Most couples opt for filing a joint return to optimize their tax refund. If marriage means a last-name change, notify the Social Security Administration so your number will coincide with your new name.

On the other hand, divorces will also affect your tax season. If you are separated or divorced, you will need to file as "head of household" if you retained custody of a child or a dependent. Lawyers.com's tax planning section shows taxpayers what to expect when filing taxes if divorced or separated.

New member of the family

Congratulations on your new addition to the family! Did you know a new child becomes a dependent on your tax forms and can give you access to the Child Tax Credit? According to TurboTax, you can save up to $1,000 per child if you meet the Child Tax Credit requirements.

Education

Being in college or having children in college can provide significant tax benefits. There are three tax credits for college students: the American Opportunity Tax Credit, the Lifetime Learning Credit and the Hope Scholarship Tax Credit. Tuition and fees also can be used as income deductions.

So, should you choose a tax credit or a deduction? The tax website efile.com says tax credits will reduce your tax bill dollar for dollar, whereas a tax deduction will only reduce your taxable income. You will need to see which credits you qualify for and then do the math to see how much you will save, but credits usually save more in taxes than deductions.

Job change

If you changed jobs or are hunting for a new job, your taxes may be affected. Any severance pay is taxable income, as well as accumulated vacation or sick time that end up as compensation, according to Kiplinger's tax planning section. If you are job hunting, any expenses relating to hiring a head hunter, traveling or printing resumes and cover letters can be deducted, as well as moving expenses, if you relocate for a new job.

Homeownership

A new home comes with new responsibilities and significant tax breaks. TurboTax suggests taxpayers take advantage of mortgage interest, real estate taxes and paid points deductions from income.

If you are selling your house, you can save up to $500,000 in taxes. To qualify for the exclusion, you must have lived in the house for two of the five years just before the sale. If you want your exclusion to be doubled from $250,000 to $500,000, TurboTax recommends filing jointly with your spouse.

Death

Even when you die, you still have to pay taxes. Fortunately, an executor will file your taxes. Your executor is responsible for paying any remaining taxes you owe and reporting all income up to the date of death. Frasier Sherman with The Nest says your beneficiaries cannot claim your estate until your executor has filed your taxes. If you receive any refunds or withholdings from the IRS, then those will go toward your estate, assuming you have no beneficiaries in your will.

New business

The first year of running your own business can be overwhelming, and those first-year tax elections can be significant. To make sure you take advantage of the benefits of self-employment, consult a tax professional about what you can deduct and what you can't.

The average American couple has retirement savings of only $5,000. Surprisingly, the flip side of their balance sheet doesn't look much better, with debts nearly tripling since 2003 for those in their mid-60s.

Older Americans aren't burning the mortgage at the retirement party. Instead, they're refinancing it, adding on 20 or 30 years of payments or drawing out cash through a reverse mortgage.

They may be borrowing to pay for a child's education, to manage the expense of divorce or the loss of a spouse, or to make ends meet after a late-career job loss. Downsizing means less space but often leads to a higher mortgage than on the original family home.

"What we see is people working longer to pay for their children's advanced education," says Todd Walter, client advisor and director of advisory services for The Joseph Group, a Columbus wealth management firm. "Their son wants to go to medical school, or even if it's not for their education, it's supporting children later on in life-whatever the kids want to do. These are people making a sizeable income, adding on a couple years of work, usually in leadership positions or management."

Unfortunately, Walter says, some older couples are repeatedly refinancing their homes, adding up to 30 years to the payoff clock and taking out extra cash. "Instead of a $100,000 mortgage, they have a $200,000 mortgage," he says.

Illness is another concern, says Patty Callahan, an information and assistance specialist at the Central Ohio Area Agency on Aging. "The health issue tends to be a big one, because that can sometimes impact two incomes in a household, the person who is injured or ill and ... sometimes the loss of income from the person serving as that person's caregiver, pulled out of employment."

Despite those concerns, a growing chorus of investment advisors to the AARP says debt is not the enemy. Instead, it has become a strategy for mature borrowers at a time of low interest rates, high home values and a relatively favorable stock market, even if they are at risk from future rate hikes.

Reverse mortgages, once a strategy for low-income elderly, are now gaining traction with high-wealth clients as a way to bolster current income without tapping into long-term savings or investment and retirement portfolios. And it's a big market.

"About 10,000 people a day are newly eligible for reverse mortgages" as they hit age 62, explains David Weinstein, national business development manager for the reverse mortgage division of Concord Mortgage Group in Westerville. "There is about $6 trillion in equity in the 62-and-over demographic."

The online Reverse Mortgage Daily reports there are $55 billion in reverse mortgage-backed securities. In October, reverse mortgage lenders issued $832 million of Home Equity Conversion Mortgage-backed securities.

In 2013 default rates on reverse mortgages peaked at 10 percent, draining the FHA Mutual Mortgage Insurance Fund, which is still $7.7 billion in deficit due to reverse mortgages. Reverse mortgage defaults prompted HUD to propose several batches of new regulations to limit immediate withdrawals and bolster credit quality.

Although reverse mortgage defaults have eased somewhat, nobody can predict exactly where that market will lead, let alone what the overall wave of debt will mean for older Americans, but there's no escaping its tsunami-like growth curve. Many moderate investment experts, sensing the difficult risk/reward equation, are taking a careful look.

"We're saying you want to be debt-free, pay off the loan and let the markets take care of themselves. That's how I'm counseling clients generally," says Walter of the Joseph Group. "Some clients are more debt-averse and saying at 60 years old, with the kids out of the house, 'I'm using all my surplus to pay off the (debt).' They may even tie their retirement to the date, roughly, when the mortgage is going to be paid off."

"Borrowing wisely is every bit as important to your financial success as investing astutely. Taking the time to structure your liabilities with the same care you place in structuring your investments can ensure a balanced approach to achieving your financial goals," says Kathleen E. Lach, senior vice president-wealth management for the Columbus office of UBS Financial Services Inc.

Other observers see baby boomers, most of them retired or moving into retirement age, taking on more than their fair share of liabilities-and risk-as they reach their golden years.

Between 2003 and 2015, aggregate debt for 65-year-olds has climbed 170 percent, and 65 percent of that growth appears to have come as boomers are hitting their 60s, according to census and Equifax data analyzed by Liberty Street Economics in a report called "The Graying of American Debt."

What's really happening is that individuals are making decisions to borrow more often, and for larger amounts. For example, those 65 and older owing money on their homes climbed from 22 percent to 30 percent from 2001 to 2011, the most recent census data shows.

In 2014, the Consumer Finance Protection Bureau says mortgages constituted 32 percent of their complaints from those 65 and over, while reverse mortgages were only 2 percent.

Despite the debt patterns, AARP-Ohio cites the early 2016 EBRI Retirement Confidence Survey, which concludes most Americans don't describe their debt as a major problem. The study says just 15 percent of workers and 8 percent of retirees believe their level of debt is a major problem, and 67 percent of retirees claim they do not have a debt problem at all.

Rather than pay off the mortgage and pay off all the credit cards, older Americans-even in high-wealth situations-are letting debts ride. Some want to sustain travel and affluent lifestyles; others borrow to preserve liquidity while they keep savings, investments and retirement accounts intact.

For most older people, though, AARP Ohio wants to emphasize savings and the need for reforms to bolster Social Security, cautioning that "increasing amounts of debt can threaten long-term financial security," especially when unforeseen illness, job loss or death of a spouse add to the burden.

"Debt does seem to be less of an issue or concern than before the recession," says Barbara Sykes, Ohio director for AARP. "But what we find is a significant number of individuals do not have retirement savings. They're not choosing to save."

That choice between borrowing, spending or saving looks more complex right now, and it takes great care to make the right call.

"Given the current interest rate environment, which in most cases still remains near historic lows, it is a good idea to review your overall debts (or liabilities) at least once a year," says Lach of UBS. "Some debts may be consolidated, some paid off and some refinanced. However, just because you can refinance or pay off debts doesn't mean you should. As a general rule of thumb, your monthly debt payments should be less than 40 percent of your monthly income."

Keeping debt under control-and in proper perspective-at retirement could be one of the most beneficial resolutions of all.

It's common for taxpayers to wonder how likely it is that their tax return will be audited, as the prospect of an IRS tax audit is rather worrisome. Here are three bits of good news, though: It's very unlikely that you'll be audited, there are ways to decrease your odds further, and even if you are audited, it's not likely to be too traumatic.

An IRS tax audit: What are the odds?

According to the 2015 IRS data Book, there were about 147 million individual tax returns filed in 2014. Of those, a sizable 1.2 million ended up "examined" -- i.e., audited. Take heart, though, because although 1.2 million is a big number, 147 million is far huger: Overall, less than 1% -- a mere 0.8% -- of the returns were audited.

Here's even more encouragement: According to IRS Commissioner John Koskinen in a March 2016 speech, relentless budget cuts by Congress has left the IRS less effective, with more than 5,000 fewer people since 2010 "who audit returns and perform collection activities, as well as... investigate stolen identity refund fraud and other tax-related crimes." He added, "As you might imagine, these staffing losses have translated into a steady decline in the number of individual audits over the past six years. Last year, in fact, we completed the fewest audits in a decade.... That trend line of fewer audits will continue this year." Clearly, if you're wondering, "Will I be audited by the IRS?" -- the answer is most likely, no.

The budget cuts are not actually a good thing, though, because fewer audits mean fewer dollars collected that were due to the government. Per Koskinen, "Historical collection results suggest that the government is forgoing more than $5 billion a year in enforcement revenue, just to achieve budget savings of a few hundred million dollars."

Make an IRS tax audit even less likely

Your odds of being audited are quite low -- but you can reduce them further in several ways. For example:

Don't fail to file a return. If you don't file a tax return for any reason, the IRS may contact and question you. Even if you had no income in the tax year or had no taxes due, you still need to file a return, explaining that you have no income and/or demonstrating that you have no taxes due.

Try not to have no income. Your odds of being audited are higher if you report no income -- even if you've filed a return. For example, if you have your own business and you posted a net loss for the year, the IRS might want to double-check to make sure you're not pulling a fast one. In 2014, about 5.3%of returns with no income were audited.

Don't omit information. If you fail to report any income or omit any other information, that can raise flags at the IRS and get you audited. Even if it's just a tiny dividend payment you don't want to bother mentioning, it needs to be included -- not only because it's the right thing to do, but also because the IRS probably already knows about it and will wonder why you haven't mentioned it. Entities that pay you -- whether it's salary payments, dividend income, interest paid, or something else -- generally report having done so to the IRS. The IRS then expects your return to include all of these payments.

Don't be messy. Your odds of being audited can rise if your handwriting is hard to read. The IRS needs to be able to make sense of your tax return, and if it can't tell whether that's a 0 or a 6, or your return is just too hard to read, it will draw attention. Avoiding audits involves trying to avoid having any attention drawn to your return. You want it to be one of millions that smoothly gets processed without question.

Don'tmake math mistakes or other mistakes. Double-check your calculations and be sure that any numbers you're entering in your return are correct. Enter the right numbers in the right boxes. It can be very helpful to use tax-preparation software and to electronically file your return, as such returns can be more accurate than hand-prepared ones. Remember to sign your return, too: Unsigned returns also draw the attention of the IRS.

Don't be dishonest. If you're stretching the truth on your tax return -- especially if you're self-employed -- you may catch the attention of auditors. Be ready to substantiate any claims (business meals, business-related miles driven, business entertainment costs, etc.) with receipts or other documentation. If you're claiming a home-office deduction, you'd better actually have a home office, and one that conforms to the rules, such as being used solely for your business.

Don't use a problematic tax preparer. If your tax return is prepared by your well-meaning uncle, you could end up audited if he makes mistakes. Professional tax preparers can make mistakes, too, of course. Unscrupulous ones can be committing fraud with your return in order to lower your taxes, or they can even be stealing from you. Ultimately, you're the one responsible for your tax return. Still, consider using a qualified preparer, as a good one will be much more informed about tax laws, available tax breaks, and strategies you might employ. A good tax pro can serve you well and reduce your tax bill.

What if you're audited anyway?

Despite all your precautions, you may still end up audited -- either due to factors out of your control or perhaps just due to chance. For example, self-employed folks and those with very high incomes are audited more often than more typical taxpayers. Those with deductions of unusual size can also trigger audits, because the IRS will generally compare the numbers in your return with averages. If you're claiming a much bigger deduction for charitable donations than the average taxpayer with your income profile, that will draw attention.

Even if an audit happens, though, don't freak out. It's very often a relatively minor event. About 70%or more of audits are conducted through the mail, not by requiring you to sit across a desk from an IRS agent. And many of them result in additional money coming your way, too. Audits can seem scary but they're not usually a problem if you've been honest.

So stop worrying about being audited: An IRS tax audit is not likely to happen, there are steps you can take to make it even more unlikely to happen, and even if you are audited, it's not likely to be too terrible an experience.

Forget worms. When it comes to taxes, the early bird gets the largest refund (and the least stress).

While it's tempting to procrastinate when it comes to filing your taxes, January is actually an ideal time to get a jump-start on the process, experts say. "History would suggest that the closer you get to the filing deadline, the more rushed you feel – [there's] more pressure and more potential for errors," says Glenn Brown, a senior tax research analyst of The Tax Institute at H&R Block in Kansas City. "If you want to maximize your return, you should file early."

Consider taking these steps in January to get a head start on your taxes.

Decide how you'll file. Take the start of the year to decide how you'llfile your taxes. Are you going to submit your tax forms electronically? Will you meet with a tax professional? "At least you know your course of action," says Barbara Weltman, an attorney and contributor to "J.K. Lasser's Your Income Tax 2017: For Preparing Your 2016 Tax Returns."

Take note of what's changed this year, says Jon Ulin, certified financial planner and managing principal of Ulin and Co. Wealth Management in Boca Raton, Florida. Did you buy or sell a house? Have a kid? Get married? Change bank accounts? Get an early look at what these milestones will mean for your taxes this year before the early-April crunch.

Call your tax preparer. If you're choosing to enlist help from a tax professional, schedule your appointment early, experts say. "Don't wait," Weltman says. "Professionals get busy."

Wait until late March or early April and your tax preparer's calendar may be booked. Scheduling early will also buy you time if you need to schedule a follow-up meeting after you, say, show up without all the necessary paperwork.

Organize your paperwork. Take the relative calm of the first month of the year to get your paperwork in order, experts say.

Gather receipts, proof of charitable contributions and other tax forms in one place. Check your mailbox every day for essential forms. If you're missing something that should have already arrived, use this time to reach out to the organization. Weltman recommends keeping everything in a single three-ring binder for easy access during filing season.

Boost your contributions. Eligible filers who submit their tax return early enough can use their refund to further reduce the previous year's taxes. "You can make an IRA or health savings account contribution for 2016 up to the due date for the 2016 return, which is April 18," Weltman says. "You have to file early enough or else the refund won’t come back in time."

This is a savvy move, for example, for qualifying filers who haven't reached their IRA limit of $5,500 (or $6,500 for investors who are 50 or older). "If you get your refund early enough, and you can input some cash into an IRA before the filing deadline, that does give you the ability to stretch out your investment there," Brown says. The amount you'll save depends on your income tax rate. For example, an eligible filer in the 25 percent bracket who invests $5,500 in an IRA for 2016 will reduce their tax bill by $1,375.

Make sure to tell the account custodian the year in which you plan to apply your refund, Weltman says. If you skip that step, he or she may earmark it for your 2017 contributions instead.

Take note: The Internal Revenue Service won't issue refunds for filers who claim the Earned Income Tax Credit or the Additional Child Tax Credituntil Feb. 15, 2017(and the refund won't land in bank accounts until the week of Feb. 27). Still, the earlier you file, the more time you have to cash in on this strategy.

Think ahead. Taking care of 2016 taxes early will give you the time to start thinking about how you'll tackle your 2017 taxes. You can use the first quarter to harvest tax losses, prepare your return for other uses, like applying for a mortgage, or adjust your withholding.

Says Weltman: "The sooner you get started, the less pressure or anxiety you'll feel."

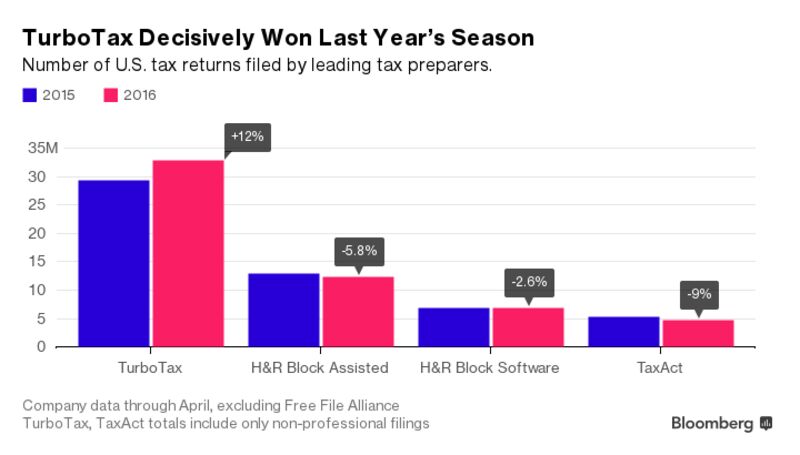

TurboTax battles H&R Block for dominance in tax preparation, while smaller players fight over the rest of the market. Despite the fierce competition, your return should end up looking more or less the same, no matter which service you use. Unless you're wealthy and have a complicated tax situation, your refund should be the same size, too, whether you secure it with a do-it-yourself online service, a storefront preparer, or a fancy accounting firm.

(This assumes that your tax preparer is competent or, if you go online, you don’t make costly mistakes using tax software—not necessarily safe assumptions.)

So the main battleground is price. In 2017, the word of the year is “free.” There are, in fact, good deals to be had, especially if you file your taxes early. The Internal Revenue Service officially began processing returns on Monday.

The trend could hurt profits in the tax prep business, said Oppenheimer & Co. analyst Scott Schneeberger. The tax season is “going to be so hyper-competitive that no one is going to have a great year,” he predicted. The big players are also spending heavily on marketing, with H&R Block hiring Jon Hamm and TurboTax, owned by Intuit, enlisting David Ortiz and Kathy Bates. Adding to the competitive pressures is a new player: The credit-monitoring website Credit Karma just started offering free tax preparation.

As for the consumer, caution is in order. Free doesn’t always mean free.

Tax preparers promise free work on simple returns to get new customers in the door. Taxpayers planning to pay nothing may soon feel the pressure to upgrade. Online tax preparers may charge additional fees for important services such as accessing or importing last year’s return and asking tax questions over the phone. Even as TurboTax spent the last couple of years winning over customers with its “absolute zero” campaign, many customers paid much more than zero. While some do get free tax advice, TurboTax managed to earn an average of $49 per U.S. return in 2015 and 2016, up from $47 in the years before.

The bottom line: If you have a simple tax return, you can probably file truly free of charge through any of the major tax preparers online. Seven in 10 Americans can use tax software through the Free File Alliance, a partnership between the IRS and a dozen tax preparers. The only requirement is an adjusted gross income of $64,000 or less.

For those with more complicated situations, figuring out the best option—the cheapest tax advice that also suits your needs—can require some digging.

Here’s a review of how the top online players—TurboTax, H&R Block, and TaxAct, now joined by Credit Karma—are positioning themselves for the 2017 tax season.

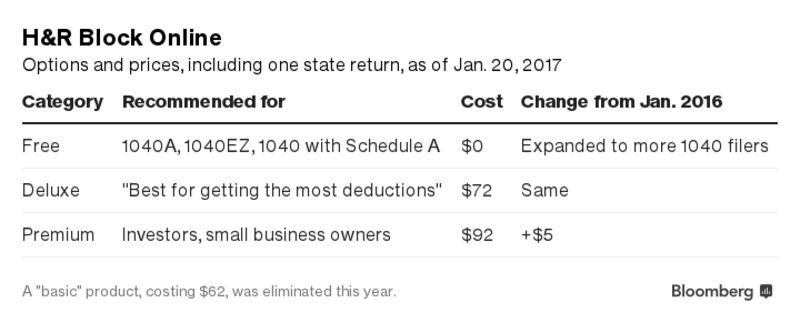

H&R Block

The “big change this year” is H&R Block, said Wedbush Securities analyst Gil Luria. “This year they’ve decided to be very aggressive.” The company made more taxpayers eligible for free tax filing, both online and in its 12,000 storefront offices, and is luring customers with a new refund product.

Why? H&R Block’s chief executive officer is blunt. “We did not have a good year” in 2016, CEO Bill Cobb said in an interview this month. “Everything that could go wrong did go wrong.”

H&R Block processed almost a million fewer returns in the U.S. in fiscal 2016 than in 2015, a 4.5 percent drop to 19.7 million, according to results reported in June.

To combat TurboTax’s “absolute zero,” H&R Block’s 2017 strategy is “more zero.” TurboTax and TaxAct will file basic tax returns—the 1040EZ and 1040A forms—for free. Online, H&R Block is matching that while also filing some regular 1040 forms free of charge, including those for homeowners with home mortgage interest deductions and real estate taxes.

Block’s biggest line of business is off-line. To attract millions of additional Americans to its offices, where it can charge more by offering one-on-one tax help, it is dangling two big lures this year.

The company is offering to process 1040EZ forms for free in person, down from about $50 last year. And taxpayers who show up may be eligible for an advance on their tax returns.

Changes to federal law and IRS procedures mean it could take until late February for early tax filers get their refunds. That can feel like a long time for low- and middle-income families that depend on large refunds, especially from the earned income tax credits and additional child tax credits that involve the longest waits. H&R Block’s Refund Advance program offers filers up to $1,250 of their refund in the form of a no-interest loan.

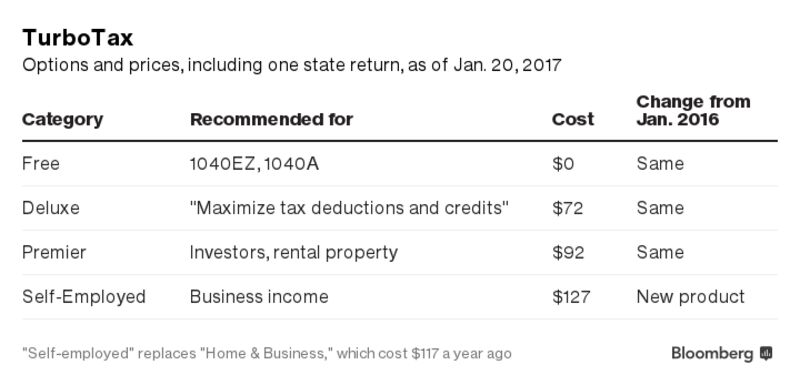

TurboTax

H&R Block’s pain last year was its archrival’s big gain. The division of Intuit decisively won last year’s tax season, with consumer tax revenue up 10 percent in the 2016 fiscal year and U.S. tax filers up 12 percent.

Not surprisingly, TurboTax is more or less sticking to its 2016 strategy. “Our pricing and value proposition is pretty consistent, year-over-year,” said Intuit spokeswoman Julie Miller. For simple filers, the “absolute zero” campaign offers free federal and state 1040EZ and 1040A returns. Those with more complex returns generally will pay more than if they had chosen discount online tax preparers such as TaxAct, though they’ll probably pay a lot less than if they hired someone to do their taxes for them.

In exchange for higher fees, TurboTax customers get higher technology. “We’re really driving a lot of product innovation,” Miller said, citing features such as video chat with tax experts. The company has also focused on shortening the amount of time it takes customers to prepare their taxes through the TurboTax site and apps.

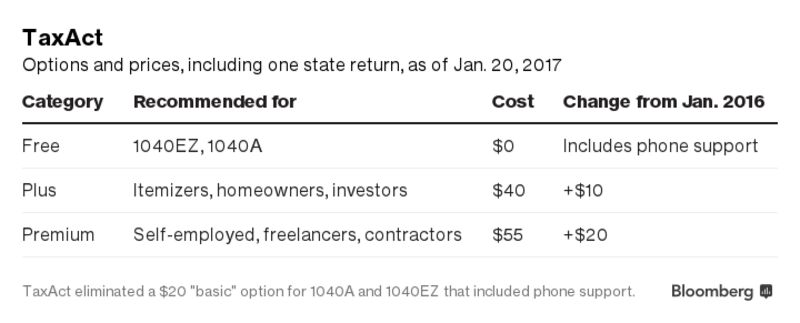

TaxAct

TaxAct, TurboTax’s much smaller rival, generally tries to charge at least 50 percent less than Turbo, with pretty basic technology and design. “We’re really focused on delivering the best value for customers,” TaxAct spokeswoman Shaunna Morgan said.

Nonetheless, this year TaxAct has raised prices. Its “plus” product, aimed at taxpayers who itemize, is starting the tax season at $40 (including both state and federal returns), up $10 from last year. That compares to $72 for TurboTax and H&R Block’s “deluxe” products.

Though TaxAct can’t price itself lower than “absolute zero,” it is trying to make its free product more attractive. This year, for example, it’s offering phone support to simple filers for no charge.

TaxAct is also promising an “upfront price” with “no shady fees.” That means disclosing on the opening screen, for example, that its “free” product includes a $5 fee to import last year’s return. TaxAct argues that it’s being more transparent about the final price you'll pay. And if you start a TaxAct return early in the tax season, you lock in that price. That protects you from increases that are common to all online players late in the season.

Credit Karma

One tax preparation service that won’t be charging any hidden fees is Credit Karma, now promising to do Americans’ taxes completely free. The credit-monitoring site makes money through advertising recommended financial products to consumers.

It’s not the first company to try to enter the online tax prep market with a free or very cheap product, and those historical examples show it won’t be easy, Wedbush’s Luria said. It’s hard for an upstart to attract enough customers. “People need to know the product works,” he said. “They need some confidence that the software can handle their taxes.”

Credit Karma founder and CEO Ken Lin is trying to win over skeptics. To launch the product, the company bought a small tax prep outfit and is hiring hundreds of preparers to offer support by online chat, e-mail, and phone.

One advantage Credit Karma enjoys is its popularity. It has more than 60 million members. Earlier this month, 1.7 million people signed up for a waiting list for tax prep, Lin said. The tax product was opened to the broader public on Monday, just as the IRS officially opened for business.Still, the product won’t address the needs of about 10 percent of taxpayers, Lin said. The software won’t be able to help people with especially complicated situations, such as those with farm income or multi-state tax returns. And there are trade-offs. Tax filers will have to register for Credit Karma, and while Lin said the company doesn’t sell customer information to advertisers, it does recommend ads to users, based on their personal financial data. The site will use your tax information to improve those recommendations, Lin said, though filers with privacy concerns can opt out by declining to "sync up your tax info" early in the process.

That's when the Internal Revenue Service will start accepting electronically filed tax returns. We have until April 18 to file returns but many file earlier in the season, if they're expecting large refunds.

The tax filing deadline this year is Tuesday, April 18, instead of the traditional April 15, because of some quirks of the calendar. April 15 is a Saturday. But the deadline won't be shifted to Monday, April 17, because that is Emancipation Day, which is celebrated in Washington, D.C.

What do tax filers need to know this season? 1. Get an appointment if you want to talk to someone at IRS offices.

Don't expect to drop into an IRS office to get any help this tax season. All offices are appointment-only now.

If you need to visit an IRS Taxpayer Assistance Center in person, you must schedule a time by calling 844-545-5630 for the appointment hotline.

Taxpayers are asked to check IRS.gov for the days and hours of service, as well as the services offered at the location they plan to visit.

2. Beware of a new hurdle if you've used a special Individual Taxpayer Identification Number.

Some tax filers will be unable to file their federal tax returns if they do not update Individual Taxpayer Identification Numbers. Warning: Any ITIN that has not been used in the past three years will no longer work for filing that return.

On top of that, individual tax identification numbers that have middle digits of 78 or 79 also expired this year.

Tax filers in these situations must renew an Individual Taxpayer Identification Number as early as possible because they cannot file a tax return without one.

The super-sized headache? The IRS notes that it can take up to 11 weeks during the peak of the tax season to get that number from the time you send in a renewal application, known as Form W-7, for the IRS to process the application and notify you about your status.

Why the change? A new federal law to combat fraud included the requirement that certain Individual Taxpayer Identification Numbers expired on Jan. 1.

"Anyone filing a tax return with an expired ITIN could experience return processing and refund delay as well as denial of some tax benefits until the ITIN is renewed," the IRS said online in a statement.

These identification numbers often are used by people who have tax-filing or payment obligations under U.S. law but are not eligible for a Social Security number.

3. Some struggling families will face delays for their tax refunds.

The IRS notes that more than nine out of 10 refunds will be issued within less than 21 days, which is good news.

But tax filers who benefit from the Earned Income Tax Credit and the Additional Child Tax Credit should not expect their refunds until possibly the week of Feb. 27, even if they file as soon as this week.

The reason? Congress is cracking down on tax-return related fraud. The Protecting Americans from Tax Hikes Act mandated the IRS delay issuing tax refunds for returns claiming the EITC or the Additional Child Tax Credit until Feb. 15. The move is designed to give the IRS more time to detect fraud and prevent refunds from being issued to ID thieves who file fake tax returns using such credits.

But consumers who depend on the refund cash will face extra delays, given holidays and weekends.

Another thing to note: The IRS online "Where's My Refund" tool will not show an estimated date for many tax returns involving the special credits until after Feb. 15.

"So don't panic in late January and mid-February if you don't see a refund date on 'Where's My Refund.' That's just how the tool will operate given the special circumstances with the EITC and ACTC refunds," said IRS Commissioner John Koskinen in prepared remarks in early January.

"Where's My Refund" at www.irs.gov and the IRS2Go phone app will be updated a few days after Feb. 15 with projected deposit dates for the early filers who receive the earned income credit and additional child credit.

4. Look out for high-cost, quick-cash on tax refund advances.

Tax filers might be tempted by refund anticipation loans that proclaim "no fee" will be charged. But Chi Chi Wu, staff attorney for the National Consumer Law Center, warns that in some cases, borrowers could face other higher fees for tax preparation or another product.

Advance loans are being heavily marketed this year by some firms, including H&R Block and Jackson Hewitt, in light of the new delays ahead for tax refunds for those who file those Earned Income Tax Credit and the Additional Child Tax Credit.

Jackson Hewitt is marketing for its Express Refund Advance, a loan of up to $1,300 that has no fees, a 0% annual percentage rate and no credit check. To get the loan, you will have to pay to file your taxes with Jackson Hewitt.

H&R Block began offering a tax-related loan for a limited time beginning Jan. 6. The H&R Block Refund Advance offers loans in the amounts of $500, $750, or $1,250 upfront for 0% interest.

The loan is loaded onto an H&R Block Emerald Prepaid MasterCard.

The amount of the advance will be deducted from tax refunds and reduce the amount that is paid directly to the taxpayer. Both Jackson Hewitt and H&R Block only offer the loans to customers who visit their offices and outlets; it's not available online.

5. Take a close look at that W-2 Form.

Some tax filers are going to discover that they have to deal with a "Form W-2 Verification Code."

About 50 million W-2 forms will include a 16-digit verification code that tax filers or preparers will need to add when prompted by tax software. About 2 million W-2s had such a code during the 2016 filing season.

The IRS anticipates that the verification code ultimately will be used on all W-2 forms in future years.

Again, we're looking at another hurdle to try to corral the crooks and prevent the filing of fake tax returns.

"We continue to ask the public to be vigilant because the scamming doesn't stop," said Luis D. Garcia, IRS spokesperson in Detroit.

The con artists pretending to be from the IRS might reach out via your e-mail in-box, your mailbox or even knock on your front door, Garcia said.

And the crooks are going after tax preparers, too.

Earlier in January, the IRS warned that cyber criminals were pretending to be tax filers who wanted help filing their returns.

The first e-mail says something like: "I need a preparer to file my taxes."

If the tax preparer responds, a second e-mail is sent that has either an embedded web address or contains a PDF attachment that has an embedded web address.

"The tax professional may think they are downloading a potential client's tax information or accessing a site with the potential client's tax information," the IRS warned.

"In reality, the cyber criminals are collecting the preparer's e-mail address and password and possibly other information."

Oddly enough, I even got one of these phishing e-mails last week. The language was stilted and off-kilter, which can be a warning sign.

It began "Hello, CPA," which I am not.

"I need a careful and experienced high quality accountant, to handle all matters of accounting including tax preparation, IRS problem resolution, and matters expected of a CPAs to handle for Individual and Small Business," the e-mail read.

"I don't need that stereo typically dull, introverted and boring accountants, I believe in the value of partnership in business relationships."

"Find attached is my tax documents."

Love that last line. I'd love to respond: Find this attachment for a way to learn how to diagram sentences and master subject-verb agreements.

But then again, we don't want the scammers to get even better at this game, do we? Best to kill and ignore all such phishing e-mails.

Everyone is looking for ways to save money. From painting their own home to changing their own oil, Americans frequently try to do something themselves rather than pay someone else to provide that service. Often this does makes sense and does save money. However, sometimes a person can ultimately cost themselves more in time and money than if they had just hired a professional from the outset.

This is often the case when someone decides to undertake the task of preparing their own income tax returns. Individuals may think to themselves, “how hard can this be”? In addition, with the widespread publicity of tax preparation software that makes the preparation process look extremely easy and straight forward some taxpayers are electing to simply prepare their own returns.

There are times when this may ultimately prove beneficial, but there are circumstances where using a paid professional does make sense and can save money, time and stress. For instance, if a taxpayer has a complex tax return it generally makes sense to use a paid tax preparer. One advisor indicated that anyone who has rental property, a small business, or complex investments should consider professional help. Paying a tax professional is paying for their knowledge and experience, and not necessarily simply paying for access to their tax preparation software.

It may also make sense to use a paid preparer when there was a major event in your life last year. The tax preparation process becomes more complex when things like a marriage, divorce, or death took place in the year. You may also benefit from a paid professional if you are buying a house, having a child, or starting college. The complexity of a tax return can increase significantly through the occurrence of one or more of these significant events.

If the tax return preparation stresses you out and the idea of an audit or tax notice causes you to lose sleep then it probably makes sense to use a paid preparer. A paid preparer is there to calm your worries and to respond to any taxing inquiries that may come after the returns are submitted. A paid preparer can work with the IRS on your behalf in the event that your return is selected for audit.

If your schedule is such that finding time to prepare your own return is impossible than it makes sense to use an outside preparer to get this off of your plate and to get it done. Each year there is a learning curve to complete all of the forms and to prepare your returns. Your time may be more effectively spent in other areas and allow the paid professional to effectively and efficiently prepare the returns.

It also makes sense to use a paid preparer to assist you with long-term planning. A good tax preparer will help to identify savings opportunities for their clients and to help to minimize the tax obligation. A good tax preparer is more than simply reporting the tax information to the taxing authorities, but is preparing the return in such a way as to reduce the tax obligation. In addition, they will make suggestions to their clients concerning current and future actions that can be taken to reduce taxes and improve the individuals overall financial situation.

So, although it may appear on the surface that you will save money by preparing your own return, this is not always the case. A paid preparer can help to reduce the stress, free up your time and help to reduce your tax obligation. In addition, they will be there in the event of any audit or letters that need clarification and responding to.

The IRS can assess many types of penalties against taxpayers: late-filing penalties, late-payment penalties, estimated tax penalties, accuracy-related penalties—and the list goes on. This column summarizes common IRS penalties that tax practitioners see almost daily, and practical ways to obtain a penalty abatement.

FAILURE-TO-FILE AND FAILURE-TO-PAY PENALTIES (SEC. 6651)

Many taxpayers file a return late and/or make a payment late. The IRS sends out automated notices proposing failure-to-file and failure-to-pay penalties, often referred to as late-filing and late-payment penalties—and abates many of them.

First-time penalty abatement is an easy "get-out-of-jail-free card" for taxpayers who have a clean compliance history of filing and paying on time with no prior penalties (other than an estimated tax penalty) for the past three years. The reasonable-cause (facts and circumstances) defense can also be successful. Refer to Internal Revenue Manual (IRM) Section 20.1.1.3.2 for a list of the IRS's criteria for evaluating the most frequently raised defenses for these penalties. Death, serious illness, fire/casualty, erroneous advice, forgetfulness, and even ignorance of the law are among the defenses discussed in the IRM. In addition, other administrative waivers could apply to certain taxpayers, such as disaster victims.

Here are penalty abatement tips for failure-to-file and failure-to-pay penalties:

If a client meets penalty abatement criteria, practitioners can attach a penalty nonassertion request to a late-filed return. This way, a practitioner could potentially avoid a notice stream altogether.

Practitioners should cite applicable law and authority, including the IRM, when requesting a penalty abatement.

Under Sec. 6651(h), the failure-to-pay penalty continues to accrue but at a reduced rate when a taxpayer establishes an installment agreement. However, if a client meets penalty abatement criteria, the practitioner can request penalty abatement at the beginning of the installment agreement and again at the end (i.e., after the debt is paid in full). If the IRS removes penalties at the beginning of the agreement and the taxpayer adheres to the agreement's terms, the IRS can also remove the penalties that continued to accrue until the tax was paid in full.

Often, qualifying for relief under the reasonable-cause criteria is subjective, depending on the IRS agent who considers the case. If the IRS originally denies a penalty abatement, consider using the Office of Appeals. Appeals may come to a different conclusion based on the hazards-of-litigation standard. At the very least, Appeals officers may be more willing to negotiate and compromise than IRS agents.

Due to IRS budget cuts and service issues, more practitioners are finding relief for their clients via Appeals. It may take over a year to resolve the issue, but it can be worth the wait. Some practitioners have even seen Appeals remove penalties based on first-time penalty abatement criteria, even if the taxpayer did not exactly meet the criteria.

ESTIMATED TAX PENALTY (SEC. 6654)

Individual taxpayers must adequately withhold from their wages and/or make estimated tax payments evenly throughout the year. When they do not, the IRS may impose the estimated tax penalty, commonly referred to as the underpayment penalty.

There is no general reasonable-cause exception for the estimated tax penalty; therefore, it is often more difficult to get the penalty removed, but it is not impossible. The IRS may abate it if the taxpayer (1) proves that the IRS incorrectly charged the penalty or made an error, (2) shows that calculating the penalty under a different method reduces or eliminates it, or (3) proves that he or she meets the waiver criteria discussed in Sec. 6654(e)(3) (i.e., by reason of casualty, disaster, or unusual circumstances, or the taxpayer retired or became disabled during the tax year or the preceding year and the underpayment was due to reasonable cause and not willful neglect).

Here are penalty abatement tips for the estimated tax penalty:

It is fairly common for the IRS to credit a payment to the wrong tax period, causing an estimated tax penalty. Simply getting the IRS to move a payment to the correct year or period can save a client from paying this penalty. It is advisable to request transcripts from the IRS each year to determine how payments and refunds are applied (as well as to see all information already reported to the IRS). A practitioner likely would need to call the IRS Practitioner Priority Service line at 866-860-4259 to address any payment issues.

Be aware of the different methods used to calculate the penalty. For example, the penalty sometimes could be reduced or eliminated by using the annualized income installment method, which is often used if a taxpayer's income varies during the year, as is the case for many sole proprietors. Form 2210, Underpayment of Estimated Tax by Individuals, Estates, and Trusts, and its instructions provide more guidance on this issue.

Use the safe harbor. Individual taxpayers will avoid the penalty altogether when they pay 90% of the tax shown on the current year's return or 100% of the tax shown on the prior year's return (110% if the taxpayer had adjusted gross income greater than $150,000 ($75,000 if married and filing separately)). For corporate clients, refer to Sec. 6655.

ACCURACY-RELATED PENALTY (SEC. 6662)

The IRS may impose an accuracy-related penalty for many types of misconduct, such as negligence, substantial understatement of tax, etc. This penalty comes up frequently in an audit (almost automatically if the understatement exceeds the greater of 10% of the tax required to be shown on the return or $5,000), but it also comes up on notices, such as the common CP2000, which the IRS sends when underreported income is detected.

The accuracy-related penalty cannot be imposed if the return position being questioned meets certain tax authority standards (e.g., the "more likely than not" standard or the "substantial authority" standard), or if a taxpayer proves he or she has reasonable cause for failing to comply.

Regs. Sec. 1.6664-4 provides guidance to help practitioners determine whether clients meet reasonable-cause criteria to avoid an accuracy-related penalty. It boils down to facts and circumstances and proving that the client exercised ordinary business care and prudence.

Here are penalty abatement tips for the accuracy-related penalty:

The IRS cannot impose the accuracy-related penalty when a return position is properly disclosed, assuming that the return position had a reasonable basis (i.e., at least an approximately 20% chance of success if challenged by the IRS). Consider disclosing certain return positions with Form 8275, Disclosure Statement, or 8275-R, Regulation Disclosure Statement,where applicable.

Common reasonable-cause defenses for the accuracy-related penalty discussed in IRM Section 20.1.5 include reliance on an incorrect information statement that the taxpayer did not know or had no reason to have known was incorrect (Forms W-2 or 1099, Schedules K-1, etc.), reliance on a competent tax adviser, and an isolated computational error.

Heavily substantiate a client's reasonable-cause defense. Attach ample documentation to support the facts and circumstances and clearly spell out how a client exercised ordinary business care and prudence.

CLOSING THOUGHTS

Remember: Those who do not ask will not receive. Large, and sometimes even small, penalties are worth fighting to get removed. A simple phone call or letter may be all that is necessary to save a client thousands of dollars. And do not be afraid to turn to the IRS Office of Appeals. It is increasingly common for penalty cases to be resolved through this channel.

The AICPA Tax Section offers many resources to help practitioners obtain a penalty abatement:

IRS First-Time Penalty Abatement page: Contains guidance on first-time penalty abatement qualifications and tips on how to effectively request an abatement using the waiver.

IRS penalty abatement request letter (AICPA Tax Section member login required): Use the letter to compose a written request for penalty abatement based on the first-time penalty abatement criteria. This letter is formatted optimally for the IRS to process the request; it contains IRM citations to substantiate the relief and can help practitioners bill for their work.